Share to

Copper weekly review

Abstract: The recent mixed macro factors, weak US economic data, strong uncertainty in trade policy and market concerns about the prospects for US economic growth have caused negative news for the copper market;The Chinese Two Sessions were successfully held and sent out an optimistic signal, injecting confidence into the market and boosting risk appetite.The US dollar index broke through and fell sharply, providing momentum for rising copper prices.Copper prices rose strongly during the week, with a weekly increase of 1.86%.

1. Main domestic spot trend chart this week:

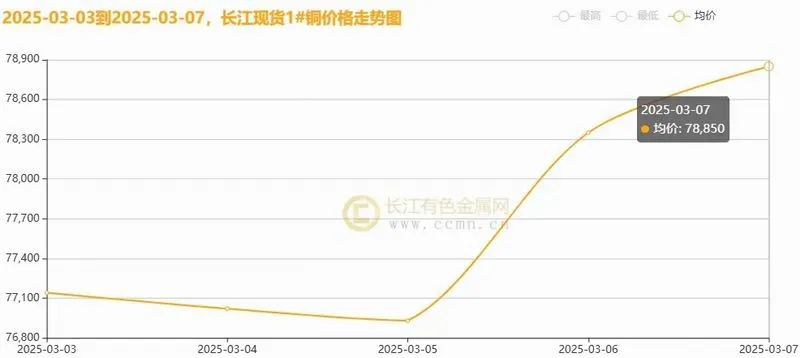

▲CCMN Yangtze River Spot 1# Copper Weekly Trend Chart

▲CCMN Guangdong Spot 1# Copper Weekly Trend Chart

3 In the week of month 7, domestic spot copper prices rose strongly.Data from the Yangtze River Nonferrous Metals Network shows that the average price of spot 1# copper in Yangtze River is 77,658 yuan /Ton, an average daily increase of 392 yuan /ton;The average price in the previous week was 77,016 yuan /Ton, the average price rose by 0.83% month-on-month last week.Guangdong spot 1# copper average price is 77,566 yuan /Ton, an average daily increase of 376 yuan /Ton, the average price in the previous week was 76,980 yuan /Ton, the average price rose by 0.76% month-on-month last week.

2. Domestic and foreign copper futures trend chart this week:

▲CCMN Lun Copper Weekly Trend Chart

CCMN Data shows that the price of London copper rebounded upward this week.The first four trading days LME The average price of copper futures is $9517.5 /Ton, an average daily increase of US$82 /ton;The average price last week was $9433.25 /Ton, the average price rose by 0.90% month-on-month last week.

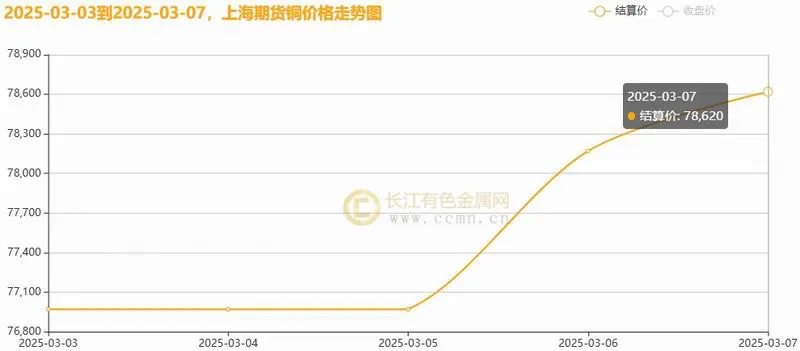

▲CCMN Shanghai copper weekly trend chart

Data from the Yangtze River Nonferrous Metals Network showed that Shanghai copper rose strongly this week, with a weekly increase of 1.86%.The average weekly settlement price of the current monthly contract is 77,540 yuan /Ton, an average daily increase of 324 yuan /ton;The average price in the previous week was 77,018 yuan /Ton, the average price rose by 0.68% month-on-month last week.

3. Domestic and foreign copper inventory trend chart:

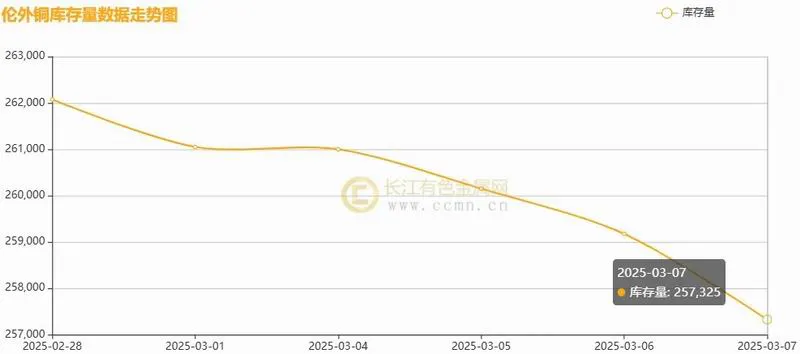

▲CCMN Lun Copper Inventory Weekly Data Chart

As shown in the above chart, London copper inventories fell this week, down 4,750 tons to 257,325 tons from the previous week, down 1.81% from the previous week.

▲CCMN Weekly data chart of Shanghai copper inventory

As shown in the above figure, Shanghai copper inventory stopped accumulating this week, showing a slight sales trend, down 961 tons from the previous week to 267,376 tons, down 0.36% from last week, but is still at a 6 and a half month high.

4. Analysis of the copper market this week:

【 Overseas news】

1、① Trump imposed 25% tariffs on Mexico and doubled the tariffs on Chinese goods to 20%, and took effect on 13:00 Beijing time on Tuesday.

② United States February ADP The number of employed people fell to 77,000, less than the expected 140,000.

③ United States February ISM manufacturing PMI It was 50.3, and the expansion tended to stagnate, inflation pressure was prominent, and the US dollar index fell sharply.

④ The number of people applying for unemployment benefits in the United States fell last week, down 21,000 to 221,000, lower than expected 233,000;The number of renewed recruits rose to 1.9 million, a figure close to the three-year high set in January this year.

2、① The ECB cut interest rates for the sixth time in nine months, with deposit rates falling to 2.5%.

② Eurozone manufacturing industry in February PMI The final value is 47.6, a record high in the past year.

③ The EU Special Summit focused on European defense autonomy and Ukraine issues, and leaders of many countries attended the meeting.

【 Domestic news】

1、①2 Yuecai New China Service Industry PMI It recorded 51.4, up 0.4 month-on-month, and the expansion of the service industry accelerated.

② Two Sessions: The reserve requirement ratio will be lowered at the right time, and the reserve requirement ratio will have room for downward space;The first batch of 500 billion special treasury bonds will be issued to support large state-owned banks in replenishing capital.

③ Minister of Finance: This year, education and social security employment expenditures are nearly 4.5 trillion yuan, and technology expenditures exceed 1.2 trillion yuan. Financial management will continue to be strengthened.

④ China National People's Congress Conference: It plans to issue 500 billion special treasury bonds to support large state-owned banks;Key industries in the Two Sessions received excess returns, and emerging themes performed outstandingly.

2、①2 From 1st to 28th, 720,000 new energy vehicles were retailed, an increase of 85% year-on-year and a decrease of 3% month-on-month, with a total of 1.465 million vehicles, an increase of 38% year-on-year.

② The government work report first mentioned "good houses" to promote the construction of safe, comfortable, green and smart residential buildings, and will continue to promote urban renewal and renovation of old communities.

③3 China's retail industry prosperity index was 50.2%, up 0.1% month-on-month;Leasing and operating categories were 51.4%, up 0.3% month-on-month;E-commerce business category was 50.1%, up 0.8% month-on-month.

④ This year's government work report proposes to increase the ultra-long-term special government bonds for consumer goods to trade olds to 300 billion yuan.

【 Supply aspect] ① Global copper mine dynamics, BHP will invest in a $2 billion plan to optimize the Escondida copper mine dressing plant, part of Chile's $10.8 billion investment plan;The hearing originally scheduled for 2025 has been postponed for six months to February 2026. The expected restart of the Cobrey Copper Mine is slim, with about 120,000 tons of copper concentrate stranded in the mining area, exacerbating concerns about tight supply in the market;The new copper mine project in Georgia is expected to be put into production from 2027 to 2028, and is expected to become the country's own Alumbrera The first large-scale copper mine project since the mine;Luoyang Molybdenum Industry, KFM Cathode copper production hit a record high.In the month, KFM The daily processing capacity of the ball mill is stable at more than 20,000 tons. ② According to the report of the International Copper Research Group, the global refined copper market was short of 22,000 tons in December, while in November, the shortage of 124,000 tons.Domestic copper concentrate supply is tight, and the negative profit value of smelters is still increasing, with a loss of 678 yuan for copper long order smelting in February /Ton, spot smelting loss of 2093 yuan /ton.It is expected that the possibility of passive production cuts will increase in the second quarter.The imported copper concentrate index fell, and the market was worried about mining and smelting contradictions.Recently, Yingtan City proposed 9 33 specific measures aimed at promoting the development of copper-based new materials manufacturing clusters and injecting strong impetus into the development of the copper industry.In addition, there is no sign of opening the import window yet, imported copper is limited, domestic supply has decreased, and some smelters have maintenance plans and increased export efforts, which brings positive support to copper prices.However, China's copper production still increases this year and may reach 12.4 million tonnes, an increase of about 4.9% year-on-year, higher than the annual increase of 3.1% in 2024.There is a negative suppression on copper prices.

【 Demand】 ①2 The transactions in commercial housing in first-tier cities and some second-tier cities rose in real estate, among which second-hand housing heated up significantly.According to CRIC statistics, 362,700 square meters of first-hand residential units were sold in Guangzhou in February, an increase of 46% and 59% year-on-year respectively.Increased supply and policies help housing prices stabilize, and the increase in improved products may attract home buyers.In this year's "Government Work Report", the "old trade-in" was mentioned again, and the "vigorously boost consumption, improve investment efficiency, and put the first place. The special government bonds that support old trade-in will increase to 300 billion yuan in 2025.Moreover, the exchange of old for new has brought new momentum for development, driving the consumption of automobiles, especially new energy vehicles, home appliances, and home decoration, to exceed 1.3 trillion yuan.As of now, there are more than 700,000 subsidies for automobile replacement and renewal subsidies, and more than 300,000 subsidies for automobile scrapping and renewal subsidies, a total of more than 1 million.BYD's sales rose by 164% in February;Overseas sales performed well, including 67,025 passenger cars sold overseas, such as 304,673 of BYD's Dynasty Ocean;Equation Leopard Auto sells 4942 vehicles;Tengshi Auto sold 8,513 vehicles;Looking up to sell 105 vehicles. ② In the terminal market, the current recovery of copper cable companies has not met expectations, and medium and low voltage orders are expected to increase in mid-March;The operating rate of fine copper rods is also slightly inferior;Although the operating rate of recycled copper has increased, the performance is not optimistic.As the "Golden March" consumption peak season enters, market consumption recovery expectations are optimistic, which supports copper prices.However, physical goods transactions are weak, buyers are not interested in restocking the warehouse, and the spot price of electrolytic copper is relatively high, which further hits the buyers' willingness to restock the warehouse.Moreover, the market premium is still at a low level, and the overall consumption mentality is relatively pessimistic.The short-term upward space on copper prices will still put certain pressure on the future.

【 In terms of spot] The spot market trading has warmed up this week, and the market's ability to take over has been enhanced, and the sentiment of holding merchants to support prices and reluctant to sell has increased.However, copper prices fell first and then rose during the week, resulting in a stronger wait-and-see sentiment in the market, weakening interest in continuing to buy goods, and overall trading activity tends to be moderate.

【 Yangtze River Viewpoint] This week's Shanghai copper futures (trading time from March 3 to March 7) has declined first and then risen, with the center of gravity of the price around RMB 76,500-78,000 /The ton range was running, and the weekly line rose by 1.86%.U.S. President Trump announced on Wednesday (March 5) that he would give some automakers a one-month tariff exemption, temporarily alleviating pressure on North American automakers and bringing a breathing opportunity to the U.S. economy, and at the same time, the U.S. in February ADP The data was unexpectedly upset, with the decline in the number of initial unemployment claims last week and Trump's trade-political measures triggering market concerns about the outlook for U.S. economic growth and inflation, causing the dollar to break through and plummet to a four-month low, making the dollar-denominated commodity prices more attractive and enhancing the investment attributes of metals.The People's Bank of China will continue to moderately loose monetary policy, and the Government Work Report puts forward economic growth and deficit targets, at 5% and 4% respectively;Accelerate the implementation of the debt replacement policy and guide local governments to issue and use this year's 2 trillion yuan replacement bond quota as soon as possible;However, the problem of commodity consumption is mainly on the demand side (the consumption willingness is weak);The main contradiction in service consumption is the insufficient supply of high-quality products.In the future, the government will attach importance to asset prices in macro-control, and for the first time, it will put the stabilization of the real estate market and the stock market into the overall requirements, promote the recovery of market confidence, heat up risk appetite in the financial market, and drive the rapid rise of copper prices.In terms of fundamentals, Panamanian President Mulino visited the country's idle flagship copper mine last week Cobre Panama, But the prospect of restart is still full of uncertainty.The interference of domestic smelting end is relatively limited. Some smelting and maintenance will be carried out in March, but regeneration and smelting have not been affected yet, and production scheduling is expected to be high.This week LME Copper inventory showed a downward trend, but overall changes were limited.The domestic inventory accumulation rate has slowed down since last week, and refined copper inventory has stopped accumulating as of this week.As we enter the third year of gold, we expect a recovery in downstream demand to be strong, and we are waiting for more positive policies to stimulate.However, the current demand is not prominent. At present, when copper prices are relatively high, downstream consumption is not willing to pick up goods, which limits spot transaction performance.However, copper prices are relatively resilient and are rising strongly as the weekend approaches. Pay attention to the pressure level at 79,000, and it is recommended to wait and see carefully.

5. International financial hotspots this week:

Domestic Finance:

1、2024 In 2019, China's economy showed strong resilience and vitality, and the economic report card has four characteristics: ① Large increments; ② High quality; ③ A solid foundation; ④ Good momentum.

2、3 On the 6th of the month, Hongmeng Zhixing announced the question of the world M9 2025 The pre-order is officially launched, with a pre-sale price starting from 478,000 yuan.Within 12 hours of pre-sale, the order volume has exceeded 13,500 units.

International Finance:

1、 New data shows that Tesla's sales in Australia plummeted 71.9% year-on-year in February this year, the entry-level Model 3 Sales volume fell by 81%, with a total sales volume of only 1,592 vehicles, and sales volume in the first two months fell by 66% year-on-year.

2、 Italy's new car registrations in February were 137,922, a year-on-year decrease of 6.3%, down 7 consecutive months.Stratlandis registration volume fell by 14%, and its market share shrank;Tesla's registration volume plummeted by 55%.

6. Looking forward to the future market:

Looking back on this week, the trend of internal and external copper futures remained resilient, and Shanghai copper futures continued to fluctuate in the high range, making it difficult to break through the 80,000 mark in the short term.The Trump administration's changing policies have exacerbated market concerns about trade prospects, while the U.S. economic data has been poor and the number of layoffs has surged, triggering market concerns about the economic slowdown.Fed Bostic said the new policy has put the US economy in turmoil and interest rate adjustments face uncertainty.The prospect of the high US dollar is worrying, and it also provides price support for the price of commodities denominated in US dollars.Chinese Finance Minister Lan Foan said that policy space will be reserved and the momentum of linking fiscal and financial policies will be strengthened.

In terms of fundamentals, after the Spring Festival, the resumption of work of domestic copper belt enterprises was slower than in previous years, resulting in limited output growth;Data released by the customs on March 7 showed that the import volume of unforged copper and copper materials in January and February this year decreased by 7.2% compared with the same period last year. The main reason is that the Spring Festival was earlier this year, and downstream enterprises began to shut down in mid-to-late January, and production was not fully resumed after the Lantern Festival (it was already mid-February);However, during this period, the demand in the spot market was relatively limited, mainly consuming in-house inventory, and the import volume was therefore not as high as the same period last year.This week entered the traditional peak consumption season "Golden Three", the market is optimistic about the prospect of consumption recovery, domestic refined copper inventory began to show signs of sales, spot discount marginally narrowed, and supply and demand fundamentals gradually strengthened to support copper prices.Copper prices will continue to remain strong in the short term;In the medium term, the shortage of copper ore supply and the growth of new energy demand will boost copper consumption, and fundamental factors will benefit copper prices.Investors need to pay attention to the US employment data tonight (March 7) to judge the economic trend.

■ Technical forecast: Copper price may be between 76,500 and 81,000 yuan next week /Ton range fluctuations.

■ Risk warning:

① US Tariff Policy: Continue to pay attention to the further development of US Tariff Policy and its impact on market sentiment.

② China's Two Sessions Policy: Policy statements during the Two Sessions will be an important observation point that affects copper prices.

③ Inventory and consumption: closely track the changes in Shanghai copper social warehouses and the cashing of downstream consumption.

ccmn.cn( The above content is for reference only, and you are responsible for the risk of entering the market based on this)

Tel

Tel Email

Email Message

Message Contact

Contact